IME India Finance Private Limited (“Company”) is a Non-Banking Financial Company – Non-Deposit Taking (NBFC-ND), registered with the Reserve Bank of India (RBI). The RBI Master Direction – Reserve Bank of India (Non-Banking Financial Company – Scale Based Regulation) Directions, 2023, applicable to Non-Banking Financial Companies (NBFCs), sets out the standards for fair business conduct and corporate practices in their dealings with customers (such standards, as modified, amended, or updated from time to time, being referred to as the Fair Practice Code).

Keeping in view the guidelines stipulated by the RBI in its said directions, the Company has formulated the Fair Practice Code (“Code”) in which principles have been carved out for fair practices/standards that the Company shall follow while dealing with its customers to build a strong relationship and foster confidence.

The Code aims to promote responsible lending, pricing transparency, ethical recovery practices, and customer rights protection across all lending products of the Company.

I. APPLICATION OF THE CODE

The Code applies to all products (including Micro-LAP/ MSME secured business loans, unsecured MSME business loans, invoice/ receivables funding, and vehicle/ asset finance (as and when introduced) and services offered across our Company’s operational and service locations, including branches, regions, and corporate offices. It is mandatory for all authorized personnel, partners, subsidiaries, and outsourcing partners to strictly adhere to the Code. This applies whether interacting in person, over the phone, by post, through interactive electronic devices, online, or by any other means.

II. APPLICATION FOR LOANS AND THEIR PROCESSING

- All communications to the borrower shall be in the vernacular language or a language as understood by the borrower.

- The Company shall transparently disclose to the borrower all information about fees/ charges payable for processing the loan application, the amount of fees refundable if loan amount is not sanctioned/ disbursed, pre-payment options and charges, if any, penal charge/ penalty for delayed repayment, if any, conversion charges for switching loan from fixed to floating rates or vice-versa, existence of any interest reset clause and any other matter which affects the interest of the borrower. In other words, the Company shall disclose ‘all in cost’ inclusive of all charges involved in processing/ sanctioning of loan application in a transparent manner. It will also be ensured that such charges/ fees are non-discriminatory.

- Loan application forms shall include necessary information which affects the interest of the borrower, so that a meaningful comparison with the terms and conditions offered by other NBFC can be made and informed decision can be taken by the borrower. The loan application form will indicate the list of documents required to be submitted with the application form.

- The Company shall devise a system of giving acknowledgement for receipt of all loan applications. The time frame for disposal of loan applications will also be indicated in the acknowledgement.

III. LOAN APPRAISAL, TERMS/ CONDITIONS & COMMUNICATION OF REJECTION OF LOAN APPLICATION

- Normally, all particulars required for processing the loan application shall be collected by the Company at the time of application. In case it needs any additional information, the customer shall be told immediately that he/ she will be contacted again.

- The Company shall convey in writing to the borrower in the vernacular language or a language as understood by the borrower by means of sanction letter or otherwise, the amount of loan sanctioned along with all terms and conditions including annualized rate of interest, method of application, EMI Structure, prepayment charges, penal charge (if any) and keep the written acceptance of these terms and conditions by the borrower on its record.

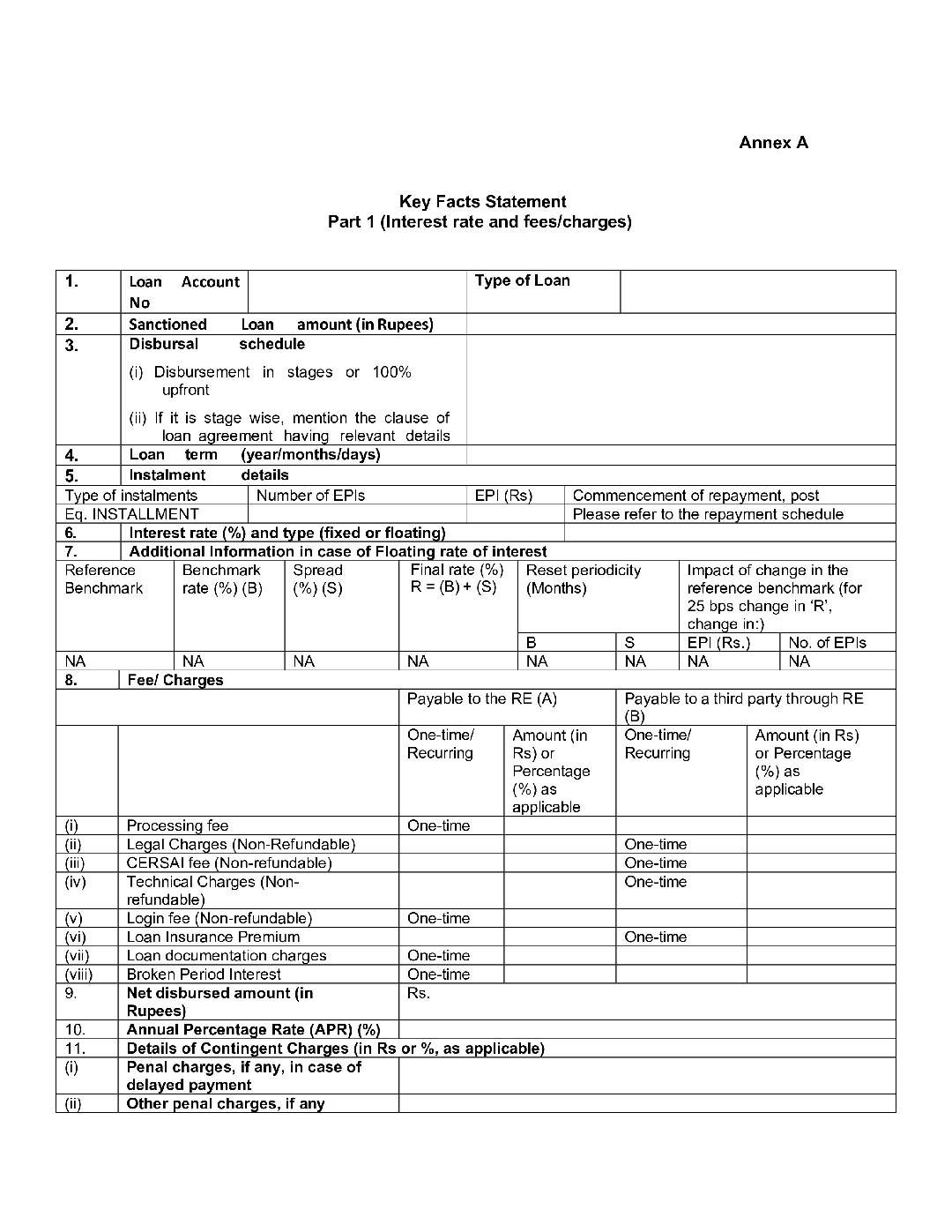

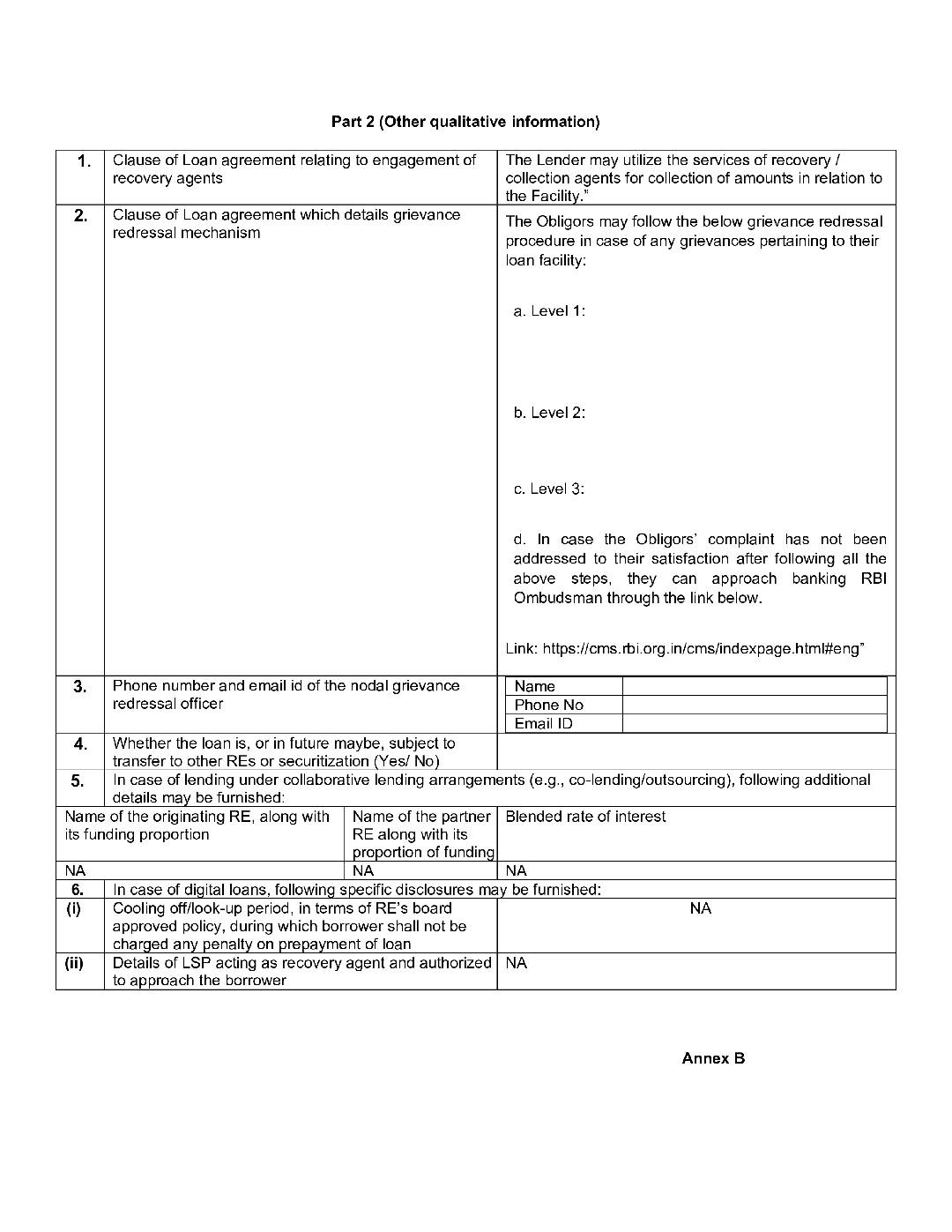

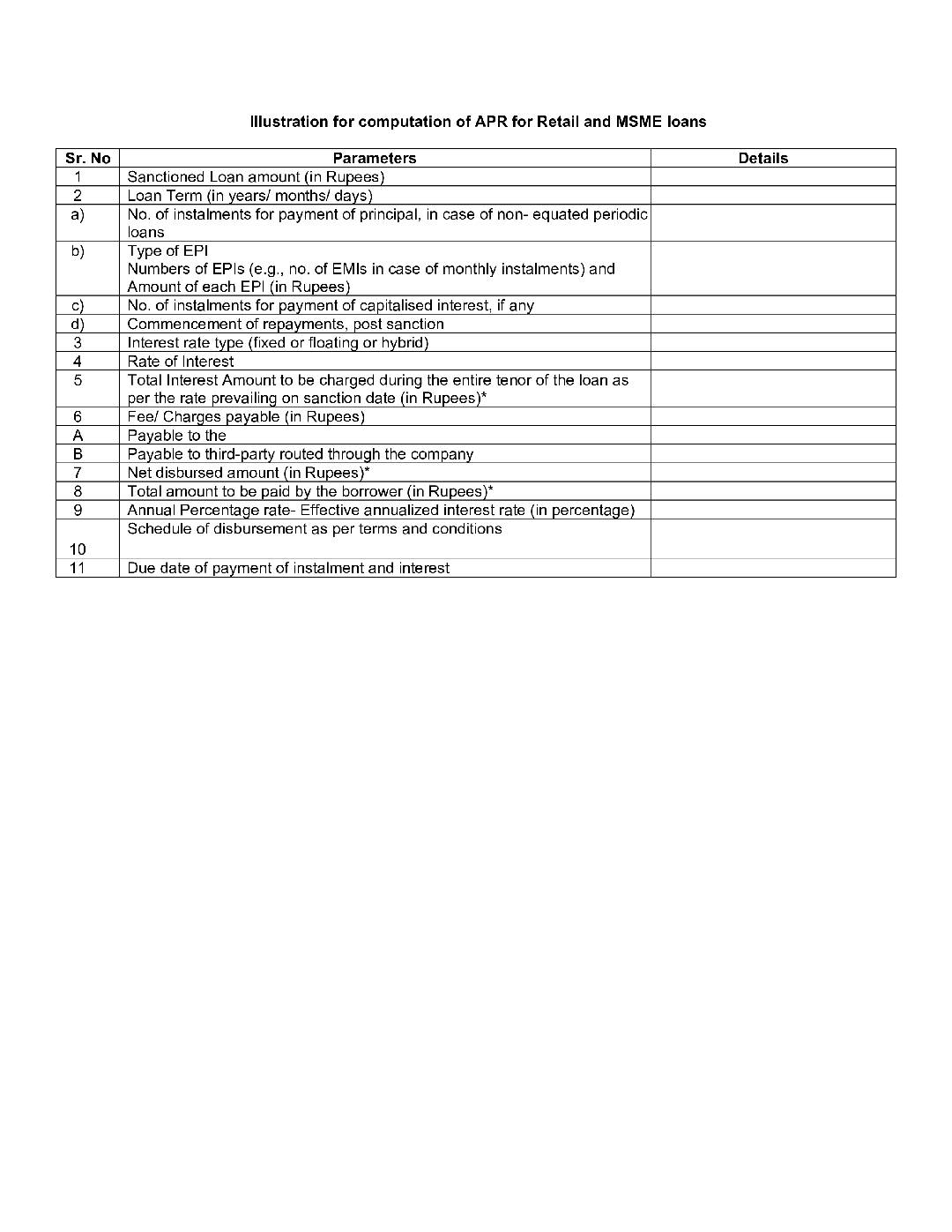

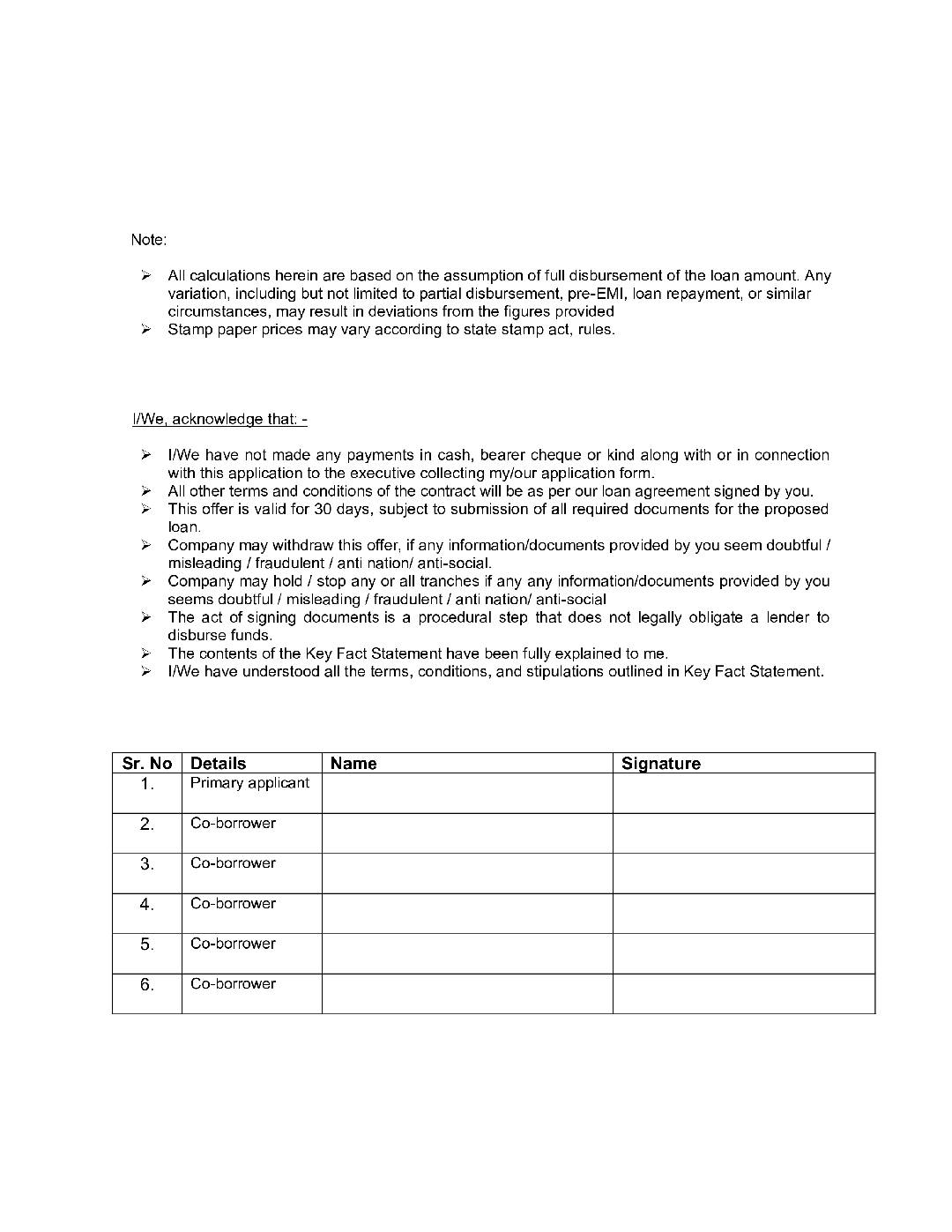

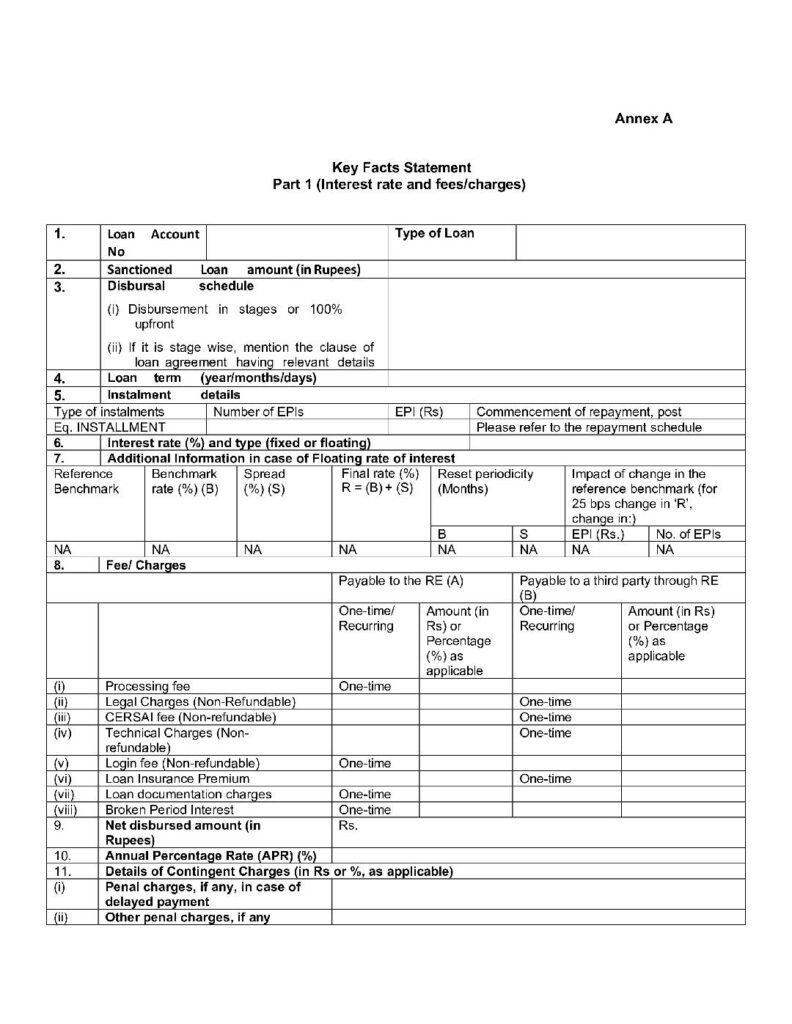

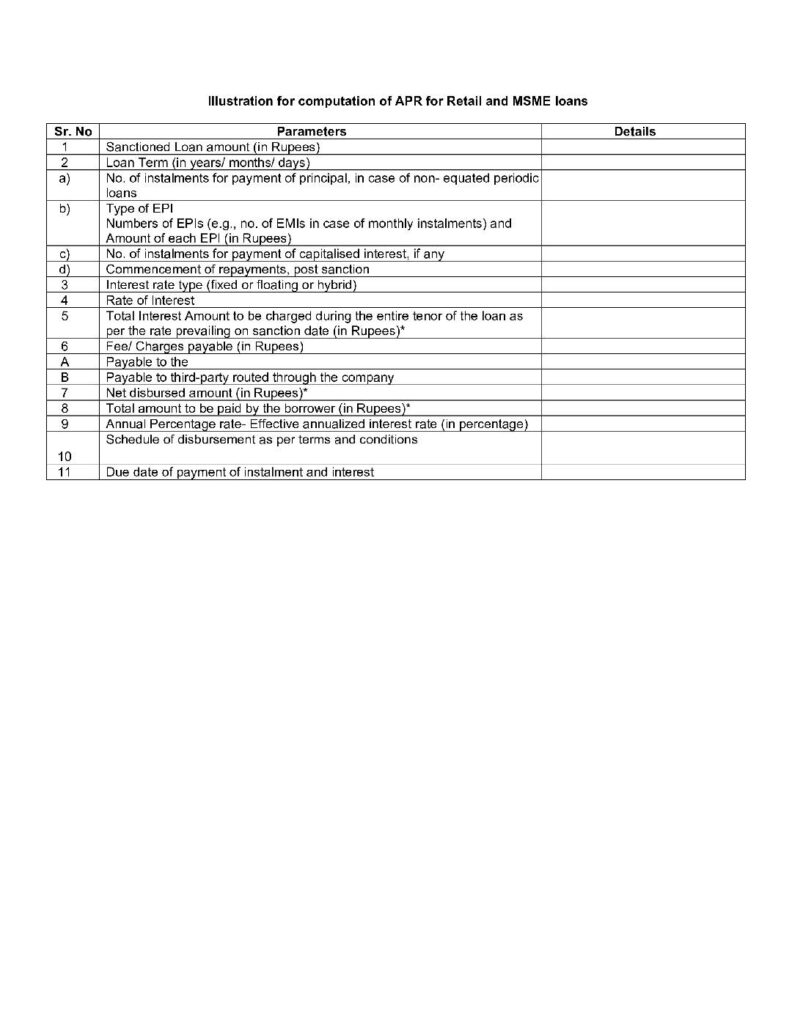

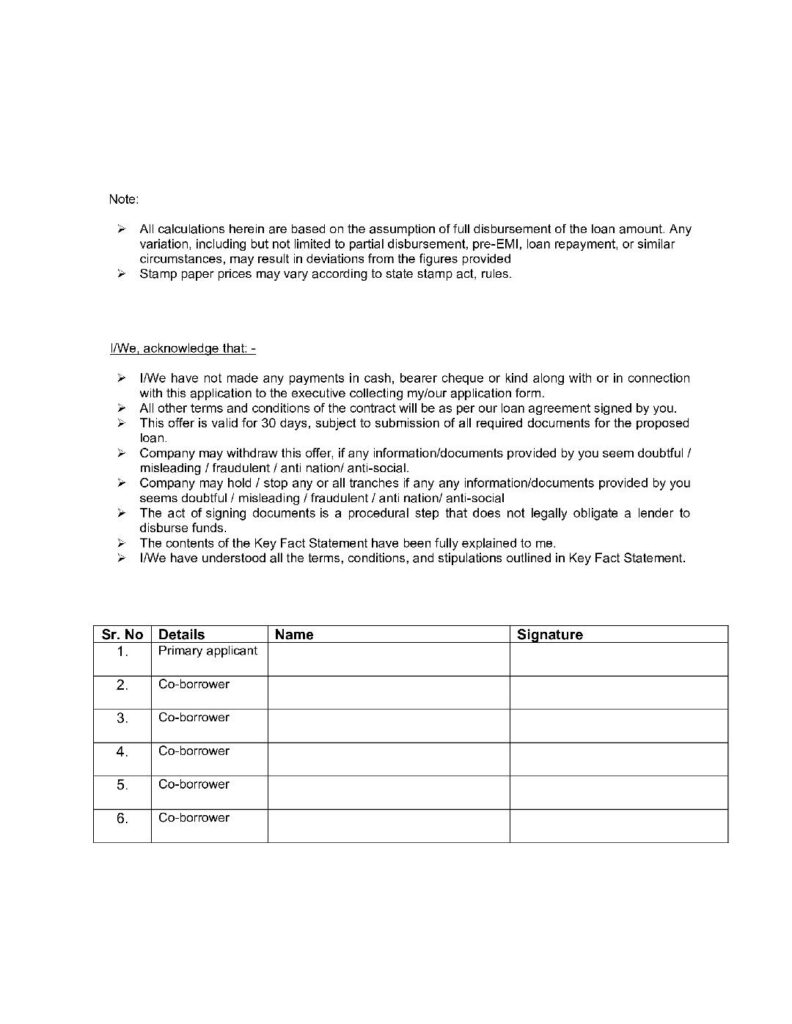

- The Company shall provide a Key Facts Statement (KFS) to all prospective borrowers to help them take an informed view before executing the loan contract, as per the standardised format. The KFS shall be written in a language understood by such borrowers. Contents of KFS shall be explained to the borrower and an acknowledgement shall be obtained that he/she has understood the same.

- Further, the KFS shall be provided with a unique proposal number and shall have a validity period of at least 3 working days. The KFS shall also include a computation sheet of annual percentage rate (APR), and the amortization schedule of the loan over the loan tenor. APR will include all charges which are levied by the Company.

- The Company shall mention the penal charges charged for late repayment in bold in the loan agree

- The Company shall invariably furnish a copy of the loan agreement along with a copy of each of the enclosures quoted in the loan agreement to every borrower at the time of sanction/ disbursement of loans, against acknowledgement.

- If the Company cannot provide the loan to the customer, it shall communicate in writing the reason(s) for rejection.

IV. DISBURSEMENT OF LOANS INCLUDING CHANGES IN TERMS AND CONDITIONS

- Disbursement shall be made in accordance with the disbursement schedule given in the loan agreement/ sanction letter.

- The Company shall give notice to the borrower in the vernacular language or a language as understood by the borrower of any change in the terms and conditions including disbursement schedule, interest rates, penal charge (if any), service charges, prepayment charges, other applicable fee/ charges etc. The Company shall also ensure that changes in interest rates and charges are affected only prospectively and a suitable condition in this regard is also incorporated in the loan agreement.

- If such change is to the disadvantage of the customer, he/ she may, within 60 days and without notice, close his/ her account or switch it without having to pay any extra charges or interest.

- Decision to recall/ accelerate payment or performance under the agreement or seeking additional securities, should be in consonance with the loan agreement.

- The Company shall release all securities on repayment of all dues or on realization of the outstanding amount of loan subject to any legitimate right or lien for any other claim that the Company may have against borrower. If such right of set off is to be exercised, the borrower shall be given notice about the same with full particulars about the remaining claims and the conditions under which the Company is entitled to retain the securities till the relevant claim is settled/ paid.

- The Company shall ensure to charge the interest to the borrower from the date of actual disbursement.

V. RELEASE OF MOVABLE/ IMMOVABLE PROPERTY DOCUMENTS

- Release of Property Documents

- The Company shall release all the original movable/ immovable property documents and remove charges registered with any registry within a period of 30 days after full repayment/ settlement of the loan account.

- The borrower shall be given the option of collecting the original movable/ immovable property documents either from the branch where the loan account was serviced or any other office of the Company where the documents are available, as per her/ his preference.

- The timeline and place of return of original movable/ immovable property documents shall be mentioned in the loan sanction letters issued.

- In order to address the contingent event of demise of the sole borrower or joint borrowers, the Company shall have a well laid out procedure for return of original movable/ immovable property documents to the legal heirs.

- Compensation for delay in release of movable/ immovable property documents:

- In case of delay in releasing of original movable/ immovable property documents or failing to file charge satisfaction form with the relevant registry beyond 30 days after full repayment/ settlement of the loan, the Company shall communicate to the borrower reasons for such delay. In case the delay is attributable to the Company, it shall compensate the borrower at the rate of Rs. 500/- for each day of delay.

- In case of loss/ damage to original movable/ immovable property documents, either in part or in full, the Company shall assist the borrower in obtaining duplicate/ certified copies of the movable/ immovable property documents and shall bear the associated costs, in addition to paying compensation. However, in such cases, an additional time of 30 days will be available to the Company to complete this procedure and the delayed period penalty will be calculated thereafter (i.e. after a total period of 60 days).

- The compensation provided under these directions shall be without prejudice to the rights of a borrower to get any other compensation as per any applicable law.

VI. RESPONSIBILITY OF THE BOARD OF DIRECTORS

- The Board of Directors of the Company has laid down the appropriate grievance redressal mechanism within the organization to resolve complaints and grievances. The mechanism ensures that all disputes arising out of the decisions of the Company’s functionaries are heard and disposed of at least at the next higher level.

- The Board of Directors of the Company shall quarterly review the compliance of this Code and the functioning of the grievances redressal mechanism at various levels of management. A consolidated report of such reviews shall be submitted to the Board on a quarterly basis, as may be prescribed by it.

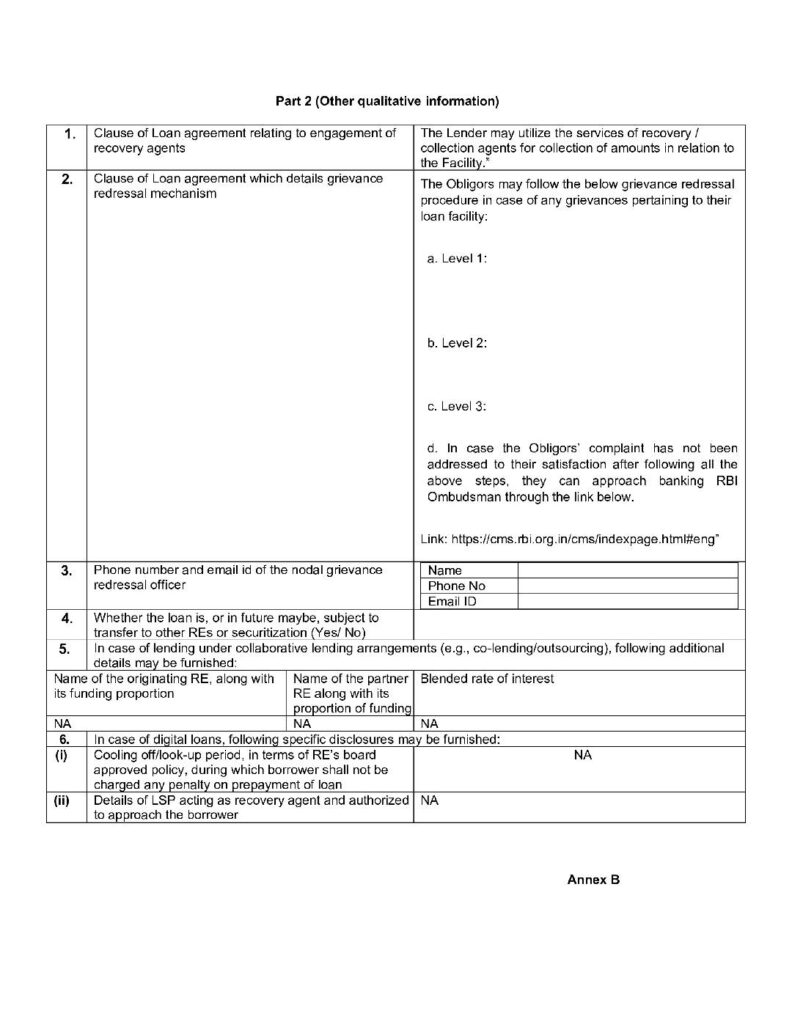

VII. COMPLAINTS AND GRIEVANCES

- The Company has a system and a procedure for receiving, registering and disposing of complaints and grievances in each of its offices, including those received on-line. If a complaint has been received in writing from a customer, the Company shall endeavour to send him/ her an acknowledgement within 2 working days and response within 7 working days. The acknowledgement should contain the name and designation of the official who will deal with the grievance. If the complaint is relayed over phone at the Company designated telephone helpdesk or customer service number, the customer shall be provided with a complaint reference number and be kept informed of the progress within 7 working days.

- After examining the matter, the Company shall send the customer its final response or explain why it needs more time to respond and shall endeavour to do so within 4 weeks of receipt of a complaint and he/ she shall be informed how to take his/ her complaint further if he/ she is still not satisfied.

- The Company has publicized its grievance redressal procedure (e-mail id and other contact details at which the complaints can be lodged, turnaround time for resolving the issue, matrix for escalation, etc.) for lodging the complaints by the aggrieved borrower and it is made available on the Company’s website.

Borrowers may register complaints through:

Email: grievance@imeindiafinance.com

Phone: 0120-4798200

Address: Nearest Branch

- If the customer wants to make a complaint, he/ she can do so:

Level 1:

- The customer may post their complaint to their branch office/ Branch business Head or by visiting company’s

- The customer shall be responded within 7 working days from the date of complaint.

- Our customer relationship management cell can be reached out through below modes:

Customer care Number: 0120-4798200

Customer care email id:

info@imeindfin.com

Website:

https://imeindiafinance.com

Level 2:

- In case the resolution is still not upto customers satisfaction, they may be approach the Grievance Officer by writing to grievance@imeindiafinance.com

- The Company’s Grievance officer shall respond within 7-15 working days.

Level 3:

If the customer is not satisfied with the resolution provided by the Company’s Grievance officer, the grievance can be escalated to the Company’s Nodal Officer at nodalofficer@imeindiafinance.com.

Level 4:

In case of non-addressal of the complaint to the customer’s satisfaction, within a month from the above quarters, the customer may approach the RBI ombudsman as per the RBI Integrated Ombudsman Scheme, 2021, as updated from time to time.

The Grievance redressal mechanism will be displayed on the notice board and will be part of the customer information folder maintained at the branch. It is made available on the website.

VIII. LANGUAGE AND MODE OF COMMUNICATING FAIR PRACTICE CODE

This Code (which shall preferably be in the vernacular language, or a language as understood by the borrower) based on the directions outlined hereinabove shall be put in place by the Company with the approval of the Board. The same shall be put up on the Company’s website, for the information of various stakeholders.

IX. REGULATION OF EXCESSIVE INTEREST CHARGED BY THE COMPANY

- The Board of the Company shall adopt an interest rate model taking into account relevant factors such as cost of funds, margin and risk premium and determine the rate of interest to be charged for loans and advances. The rate of interest and the approach for gradation of risk and rationale for charging different rate of interest to different categories of borrowers shall be disclosed to the borrower or customer in the application form and communicated explicitly in the sanction letter. The Board of the Company shall also clearly lay down policy for penal charge/ charges (if any).

- The rates of interest and the approach for gradation of risks, and penal charge (if any) shall also be made available on the website of the Company or published in the relevant newspapers. The information published in the website or otherwise published shall be updated whenever there is a change in the rates of interest.

- The rate of interest and penal charge (if any) must be annualised rate so that the borrower is aware of the exact rates that would be charged to the account.

- Instalments collected from borrowers shall clearly indicate the bifurcation between interest and principal.

IX.A PENAL CHARGES IN LOAN ACCOUNTS

- Penalty, if charged, for non-compliance of material terms and conditions of loan contract by the borrower shall be treated as ‘penal charges’ and shall not be levied in the form of ‘penal interest’ that is added to the rate of interest charged on the advances. There shall be no capitalisation of penal charges i.e. no further interest computed on such charges.

- The Company shall not introduce any additional component to the rate of interest and ensure compliance to RBI guidelines.

- The Company shall follow the Board approved policy on penal charges or similar charges on loans.

- The quantum of penal charges shall be reasonable and commensurate with the non- compliance of material terms and conditions of loan contract without being discriminatory within a particular loan / product category.

- The penal charges in case of loans sanctioned to ‘individual borrowers, for purposes other than business’, shall not be higher than the penal charges applicable to non- individual borrowers for similar non-compliance of material terms and conditions.

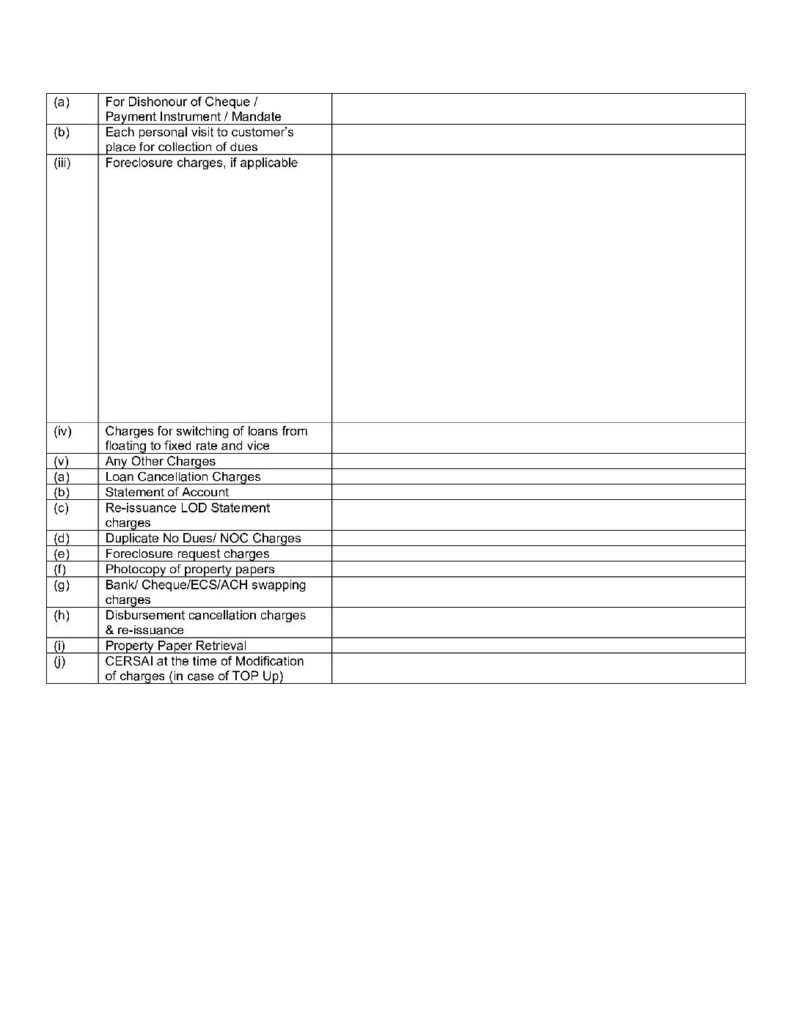

- The quantum and reason for penal charges shall be clearly disclosed by the Company to the customers in the loan agreement and most important terms & conditions / Key Fact Statement (KFS) as applicable, in addition to being displayed on the Company’s website under interest rates and service charges.

- Whenever reminders for non-compliance of material terms and conditions of loan are sent to borrowers, the applicable penal charges shall be communicated. Further, any instance of levy of penal charges and the reason therefor shall also be communicated.

IX.B RESET OF FLOATING INTEREST RATE ON EQUATED MONTHLY INSTALMENTS (EMI)

- At the time of sanction, the Company shall clearly communicate to the borrowers about the possible impact of change in interest rate on the loan leading to changes in EMI and/or tenor or both. Subsequently, any increase in the EMI, tenor or both on account of the above shall be communicated to the borrower immediately through appropriate channels.

- At the time of reset of interest rates, the Company shall provide the option to the borrowers to switch over to a fixed rate as per their Board approved policy.

- The borrowers shall also be given the choice to opt for (a) enhancement in EMI or elongation of tenor or for a combination of both options; and, (b) to prepay, either in part or in full, at any point during the tenor of the loan. Levy of foreclosure charges/ pre-payment penalty shall be subject to extant instructions.

- All applicable charges for switching of loans from floating to fixed rate and any other service charges/ administrative costs incidental to the exercise of the above options shall be transparently disclosed in the sanction letter and also at the time of revision of such charges/ costs by the company.

- Company shall ensure that the elongation of tenor in case of floating rate loan does not result in negative amortisation.

- Company shall share/ make accessible to the borrowers, through appropriate channels, a statement at the end of each quarter which shall at the minimum, enumerate the principal and interest recovered till date, EMI amount, number of EMIs left and annualized rate of interest/ Annual Percentage Rate (APR) for the entire tenor of the loan.

X. ADVERTISING, MARKETING AND SALES

The Company shall ensure that;

- All advertising and promotional material is clear and factual.

- In any advertising in any media and promotional literature that draws attention to a service or product and includes a reference to an interest rate, the Company shall also indicate whether other fees and charges will apply, and that full details of the relevant terms and conditions are available on request or on the website.

- The Company will provide information on interest rates, common fees and charges (including penal charge, if any) through putting up notices in their branches; through telephone or help-lines; on the Company’s website; through designated staff/ help desk; or providing service guide/ tariff schedule.

- If the Company avails services of third parties for providing support services, it shall require that such third parties handle customer’s personal information (if any available to such third parties) with the same degree of confidentiality and security as the Company would.

- The Company will, from time to time, communicate to customers various features of their products. Information about their other products or promotional offers in respect of products/ services may be conveyed to customers only if he/ she has given his/ her consent to receive such information/ service either by mail or by registering for the same on the website or on customer service number.

- The Company shall apply/ prescribe a code of conduct for their Direct Selling Agencies (DSAs) whose services are availed to market products/ services which amongst other matters require them to identify themselves when they approach the customer for selling products personally or through phone.

- The Company shall adopt the policy on Model Code of Conduct for Direct Selling Agents (DSAs)/ Direct Marketing Agents (DMAs) as per the approval of the Board.

- The Company will review the conduct of DSA/ DMAs annually. In the event of receipt of any complaint from the customer that the Company’s representative/ courier or DSA/ DMA has engaged in any improper conduct or acted in violation of this Code, appropriate steps shall be initiated to investigate and to handle the complaint and to make good the loss.

XI. GUARANTORS

When a person is considering being a guarantor for a loan, he/ she shall be informed about:

- His/ her liability as guarantor;

- The amount of liability he/ she will be committing him/ herself to the Company;

- Circumstances in which the Company will call on him/ her to pay up his/ her liability;

- When the Company has recourse to his/ her other monies in the Company if he/ she fails to pay up as a guarantor;

- Whether his/ her liabilities as a guarantor are limited to a specific quantum or are they unlimited; and

- Time and circumstances in which his/ her liabilities as a guarantor will be discharged as also the manner in which the Company will notify him/ her about this.

In case the guarantor refuses to comply with the demand made by the creditor /lender, despite having sufficient means to make payment of the dues, such guarantor would also be treated as a willful defaulter.

The Company shall keep him/her informed of any material adverse change/s in the financial position of the borrower to whom he/ she stands as a guarantor.

XII. PRIVACY & CONFIDENTIALITY

All personal information of present and past customers shall be treated as private and confidential and shall be guided by the following principles and policies. The Company shall not reveal information or data relating to customer accounts, whether provided by the customers or otherwise, to anyone, including other companies/ entities in their group, other than in the following exceptional cases:

- If the information is to be given by law;

- If there is a duty towards the public to reveal the information;

- If the Company’s interests require them to give the information to prevent fraud etc. Customer’s information shall not be given to anyone for marketing purposes except with his/ her permission;

- If the Customer asks Company to reveal the information, or with the Customer’s permission; or

- If Company is asked to give a reference about a Customer, the Company will obtain his/ her written permission before giving it.

The customer shall be informed the extent of his/ her rights under the existing legal framework for accessing the personal records that the Company holds about him/ her.

The Company shall not use customer’s personal information for marketing purposes by anyone including company, unless the customer specifically authorizes them to do so.

XIII. GENERAL

- The Company will refrain from interference in the affairs of the borrower except for the purposes provided in the terms and conditions of the loan agreement (unless information, not earlier disclosed by the borrower, has been noticed).

- In case of receipt of request from the borrower for transfer of the borrowal account, the consent or otherwise i.e. objection of the Company, if any, shall be conveyed within 21 days from the date of receipt of request. Such transfer shall be as per transparent contractual terms in consonance with law.

- Whenever loans are given, Company will explain to the customer the repayment process by way of amount, tenure and periodicity of repayment. However, if the customer does not adhere to repayment schedule, a defined process in accordance with the laws of the land shall be followed for recovery of dues. The process will involve reminding the customer by sending him/her notice or by making personal visits and/or repossession of security if any.

- In the matter of recovery of loans, Company will not resort to harassment viz. persistently bothering the borrowers at odd hours, use muscle power for recovery of loans etc. Company will ensure that the staff is adequately trained to deal with the customers in an appropriate manner.

- The Company shall adopt the Policy for recovery and collection.

- The Company shall not charge foreclosure charges/ pre-payment penalties on any floating rate term loan sanctioned for purposes other than business to individual borrowers, with or without co-obligant(s). In respect of loans (including term loans as well as demand loans) and advances sanctioned or renewed on or after January 1, 2026, NBFCs shall ensure compliance with the instructions issued vide ‘Reserve Bank of India (Pre-payment Charges on Loans) Directions, 2025’, dated July 02, 2025, as amended from time to time.

- All dual/ special rate (combination of fixed and floating) housing loans will attract the pre-closure norms applicable to fixed/ floating rate depending on whether at the time of pre-closure, the loan is on fixed or floating rate. In case of a dual/ special rate housing loans, the pre-closure norm for floating rate will apply once the loan has been converted into floating rate loan, after the expiry of the fixed interest rate period. This applies to all such dual/ special rate housing loans being foreclosed. It is also clarified that a fixed rate loan is one where the rate is fixed for entire duration of the loan.

- Company will not impose foreclosure charges/ pre-payment penalties on any floating rate term loan sanctioned for purposes other than business to individual borrowers, with or without co-obligant(s).

- To facilitate quick and good understanding of the major terms and conditions of loans agreed upon between the Company and the individual borrower, the Company will obtain a document containing the Most Important Terms and Conditions (MITC) of such loan. The document will be in addition to the existing loan and security documents being obtained by the Company. The Company will prepare the said document in duplicate and in the language understandable by the borrower. Duplicate copy duly executed between the Company and the borrower should be handed over to the borrower under acknowledgement. The standard format of MITC in line with the regulatory guidelines will also be made available on the website.

- Display of various key aspect such as service charges, interest rates, Penal charge (if any), services offered, product information, time norms for various transactions and grievance redressal mechanism, etc. is required to promote transparency in the operations of the Company. Hence, the Company will display the instructions on “Branch Notice Board”, “Booklets/ Brochures”, “Website”, “Other Modes of Display”.

- Company shall display about products and services offered by the Company in any of the following languages: Hindi, English or the appropriate local language.

- The Company will not discriminate on the basis of age, race, caste, gender, marital status, religion, or disability, as far as it is not in contradiction with any law of the land. However, the restrictions on age, as mentioned in the loan products, shall continue to apply.

- The Company will issue MITC updated at every stage of loan processing covering schedule of charges, changes in terms and conditions etc. in the Company’s official website besides displaying in the notice board of the branch. Company will also provide a copy on request, either over the counter or by electronic communication or email. However, this does not preclude the Company from instituting or participating in schemes framed for different sections of the society.

- Upon the specific request of the customer, the Company shall provide the facility of electronic transfer of loan proceeds through NEFT/RTGS to the account of the beneficiary/ builder/ vendor and the Company.

- The Company is having the customer portal facility on the website, and the customer can access the accounts through such facility for obtaining provisional/final interest paid certificate for IT purposes, statement of accounts etc., by properly registering the passwords.

- Generally, all the data/ documents pertaining to any account of the customer will be purged after 5 years from the closure of the loan/account and the Company will not entertain any request for providing any information/data of such accounts after 5 years.

- After disbursement of the loan and issue of a cheque in the name of the borrower/ vendor, if the purchase transaction could not be completed for whatever reasons and the cheque is recredited to the loan account, the borrower shall pay the interest at applicable rate for the period between date of debit to the loan account and closure of the loan.

- The customer should comply with the rules of Know Your Customer (KYC), Anti Money Laundering (AML), as published on our website from time to time.

- The Company would promptly attend to any “lender-related” genuine difficulty/ies that the borrowers may face. The Company will be concerned with sanction and disbursement of the loan, but will not offer any warranty for the property/ property related issues, and the borrower should satisfy himself with the title of the property, quality of the construction, progress of the project, etc.

- It is the borrower’s responsibility to register the correct postal address, e-mail ID, telephone number and mobile number and any other means of communication with the Company.

- Request for reduction of EMI shall be considered if any pro-rata reduction in the amount of EMI at the specific request of the borrower on account of bulk/ lump sum pre-payment of the loan by the borrower to keep the same tenure of the loan. In respect of prepayment, customer will have the option of reduction in EMI only in cases where such prepayment is equivalent to minimum 5 EMIs or 10% of the remaining outstanding balance.

- Whenever there is any upward revision in ROI, the Company will increase the loan tenure upto maximum permissible age. Company will inform, the borrower of the changes in his loan account and balance loan tenure. Borrower shall have the options –

- to pay the applicable enhanced EMI prospectively;

- pay applicable lump sum prepayments and continue same EMI;

- continue same EMI and extend the tenure of the loan; or

- to switch to fixed rate structure with applicable fee

- It shall be the responsibility of the borrower to visit/ contact the branch for either of the above, post the communication /changes in interest rate.

- Whenever downward revision is effected in the ROI (card rates) for loans, same is applicable for new loans granted prospectively. In respect of old loans, subject to the applicable terms, borrowers will have the option of availing the benefit of reduced interest rate by switching over to the latest Company’s finance rate and reset of ROI mode by paying a nominal fee and completion of few formalities.

- This Policy shall be reviewed annually or at earlier intervals by the Board of Directors of the Company.

- To publicize the Code, the Company shall:

- provide existing and new customers with a copy of the Code;

- make this Code available on request either over the counter or by electronic communication or mail;

- make available this Code at every branch and on their website; and

- ensure that their staffs are trained to provide relevant information about the Code and to put the Code into practice.

I.INTRODUCTION

In the present scenario of competitive banking and financial services, excellence in customer service is the most important tool for sustained business growth. IME India Finance Pvt. Ltd. (“Company”) is committed to ensuring fair treatment, transparency, dignity, and respect for all customers.

Customer grievances/complaints are part of the business of a service organisation. As a responsible corporate entity, the timely resolution of complaints and process improvements based on learnings from such complaints are the key drivers of service culture. Imparting good customer service and enhancing the level of customer satisfaction are the prime objectives of the Company. This is essential to attract new customers and to retain existing customers who are our brand ambassadors.

II. SCOPE

This document defines the grievance redressal mechanism and the policy that would be adopted to handle grievances/complaints.

III. DEFINITION

A complaint is an expression of dissatisfaction made to an organization, related to its products or services, or the complaints’ handling process itself, where a response or resolution is explicitly or implicitly expected. A complaint may also be raised against (a) delay or failure in delivering promised services; (b) miscommunication, misinformation or lack of transparency; (c) unfair charges or denial of legitimate requests; (d) harsh, rude, or discriminatory behaviour by staff; (e) technology or operational errors affecting the customer; and (f) any grievance impacting customer trust or financial harm.

The customer has the right to register his/her complaint if not satisfied with the services provided by the Company. There are four main ways to register complaint with the company – in person at branch, by telephone to contact center, by post, mobile/web application and e-mail. The complaints received through all these channels must be handled efficiently and swiftly. If customer’s complaint is not resolved within the prescribed time frame or if he is not satisfied with the solution provided by the company, the customer can escalate to the regulator.

IV. CUSTOMER COMPLAINT HANDLING PROCESS

All customer complaints received from any channel are to be duly recorded in the Customer Relationship Management (CRM) system. The complaints are categorised under three P’s, namely Person, Policy and Process after conducting a detailed analysis of the issue reported.

A. Mode of receipt of complaints

- Customer walk-in: Customers may visit our branches and lodge complaints, if required, through the Complaint Register.

- E-mails: Customers can share their grievances on email (the details of the email IDs are mentioned in the subsequent section on grievance redressal mechanism in this document).

- Phone calls: A Toll-Free number 0120 – 4798200 is available for the customer to dial in and speak to our contact center executive.

- Letters/ Physical correspondence (except addressed to BO/RBI): All physical correspondences (including the original documents), addressed to the Nodal Officer or the Senior Management, received at the published addresses of the Company.

- Website: Self-service electronic medium is made available to the customers. Customers can directly register their grievance on our website.

- Future digital grievance system as and when launched.

B. Resolution of complaints

- All escalated cases received from various sources will be recorded in the central CRM system as “cases”.

- All cases created in the central CRM system are to be queued into the central service team.

- An automated acknowledgement will be sent to the customers within a week (through email and/or SMS) stating the case reference number. An acknowledgement carrying dealing officials name and designation will also be sent to the customer (through email and/or SMS).

- The central service team to categorize the complaint in the system.

- The central service team will review the complaint and assign it to the respective branch team for resolution. If identified, the central service team will interact with the respective functional team and provide the resolution to the customer.

- For complaints referred, the branch team will interact with the customer to address his/her complaint. Post resolution, the details of the resolution are to be updated in the central CRM system and the interaction is to be assigned back to the central service team for closure.

- The central service team to examine the response and, in case the resolution is unsatisfactory, the case be assigned back to the respective unit/team responsible for resolution with relevant comments.

- After finally examining the matter, the central service team/branch to send the customer its final response or explain why it needs more time to respond and shall endeavour to do so within six weeks of receipt of a complaint.

C Time frame

The time frame of complaint resolution will depend on the nature and complexity of the issue. The Company will endeavour to resolve the complaints in minimum time frame as possible as per para VII of the Fair Practice Code to monitor and supervise the upper time limit for resolution of all escalations. Notwithstanding any timeline specified in the Fair Practice Code, the customer may be responded to as per below turnaround time:

| Type of complaint | Turn-around time |

| Simple service requests (statements, certificates, information) | 3 working days |

| Loan servicing issues (EMIs, NOC, foreclosure, delayed posting) | 7 working days |

| Complaints requiring internal investigation | 15 working days |

| Fraud / Data security / Serious disputes | 30 working days with weekly updates |

If resolution is delayed, the customer must be informed with revised timelines and interim status updates.

D. Grievance Redressal Mechanism

If a customer is not satisfied with the resolution, or if TAT is exceeded, the complaint may be escalated as follows:

- Level 1

The customer may submit the complaint through any of the modes/channels as mentioned in section IV.A above. The first point of redressal will be the service branch manager. The respective branch manager will be the first person responsible for addressing the complaint. The branch manager shall respond within 3-7 working days.

- Level 2

If the customer is not satisfied with the resolution provided by the branch manager, the customer may post his/her complaint to the Company’s Grievance officer at grievance@imeindiafinance.com. The Company’s Grievance officer shall respond within 7-15 working days.

- Level 3

If the customer is not satisfied with the resolution provided by the Company’s Grievance officer, the grievance can be escalated to the Company’s Nodal Officer at nodalofficer@imeindiafinance.com.

- Level 4

In case of non-addressal of the complaint to the customer’s satisfaction, within a month from the above quarters, the customer may approach the RBI ombudsman as per the RBI Integrated Ombudsman Scheme, 2021, as updated from time to time.

The Grievance redressal mechanism will be displayed on the notice board and will be part of the customer information folder maintained at the branch. It is made available on the website.

E. Monitoring and review of complaints

- An MIS for all the open complaints to be prepared and shared with all the stakeholders, highlighting the number of days the case is pending for resolution.

- Complaints to be periodically reviewed by the Customer Service & Grievance Redressal Committee or any other committee that the Company may have for this purpose, and the minutes to be released after the review meeting.

- Customer Service and Grievance Redressal Committee shall be responsible for:

a. regularly meet and review the position of complainants received and action taken on various complaints;

b. formulate standard responses and corrective actions to reduce the incidence of complaints;

c. evaluate feedback on the quality of customer service is followed;

d. ensure that all the regulatory instructions regarding customer services are followed; and

e. monitor the type of grievances/complaints received and corrective practices to reduce complaints.

F. Redressal of Grievances related to Outsourced Services (Recovery Agents/DSA/DMAs/IT Vendor)

- Issues related to services provided by the outsourced agency will be handled appropriately under the grievance redressal mechanism, as explained above.

- Generally, a time limit of 30 days may be given to the customers to prefer their complaints/grievances. In the event of receipt of any complaint from the customer that the Company’s representative/courier or DSA has engaged in any improper conduct or acted in violation of this Policy, appropriate steps will be initiated to investigate and to handle the complaint and to make good the loss. The respective vertical will be informed to take appropriate action.

- Complaints received by the Company regarding violation of the code of conduct for recovery agencies, would be viewed seriously.

- Where a grievance/complaint has been lodged, the Company shall not forward cases to recovery agencies till grievance/complaint lodged by the concerned borrower has been disposed. However, where the Company is convinced, with appropriate proof, that the borrower is continuously making frivolous/vexatious complaints, it may continue with the recovery proceedings through the recovery agents even if a grievance/complaint is pending. In case the subject matter of the borrower’s dues might be sub judice, the Company shall exercise utmost caution, as appropriate, in referring the matter to the recovery agencies, depending on the circumstances.

G. Complaints from Persons with disabilities

All channels will be available for persons with disability to register their grievance. For walk-in customer’s, required assistance will be provided by the Customer Service Manager. The Company shall ensure redressal of grievances of persons with disabilities under the Grievance Redressal Mechanism as explained above.

V. Maintenance of Records

The record of each grievance/complaint received by the Company and the measures taken for its redressal shall be preserved for a minimum period of 8 years from the date of resolution.

VI. Dissemination of Policy:

This Policy shall be hosted, in public domain, on the website of the Company.

VII. Mandatory display at branches:

- Name, address and contact number of Grievance Redressal Officer(s) is made available on public domain.

- This Policy is printed on sanction letter / MITC / Fair Practice Code / website / branch display boards for information.

VIII. Review:

This Policy may be amended, modified or supplemented from time to time to ensure compliance with any modification, amendment or supplementation to the applicable laws from time to time. The Policy shall be reviewed at least annually or as and when required by the applicable rules and regulations.

Interest Rate Model and policies and procedures for determining Interest Rates and other charges

Preface

As per Reserve Bank of India (“RBI”) Master Direction – Reserve Bank of India (Non-Banking Financial Companies – Responsible Business Conduct) Directions, 2025, vide RBI/DOR/2025-26/362 DOR.MCS.REC.No.281/01-01-039/2025-26, dated November 28, 2025, the Board of Directors of all Non-Banking Financial Companies (“NBFCs”) shall adopt an Interest Rate Model taking into account relevant factors such as cost of funds, operating costs and risk premium etc., and determine the rate of interest to be charged for loans and advances.

And rates of interest and the approach for gradation of risks shall also be made available on the website of the companies.

Keeping in view the RBI’s guidelines as cited above, and the good governance practices being followed by IME India Finance Private Limited (IME India Finance), the following internal Guidelines, Policies, Procedures and interest rate model have been adopted by the Board of IME India Finance at its meeting held on 21st January, 2026, for its lending business.

These need to be taken cognizance of while determining interest rates and other charges, and changes thereto.

Methodology

- The interest rates for each of our products are decided by the Board. The average yields and the minimum rate of interest under each product is decided from time to time, giving due consideration to the following factors;

- The weighted average cost of borrowed funds as well as costs incidental to those borrowings, taking into consideration the average tenure, market liquidity and refinancing avenues.

- Cost of servicing the equity capital.

- Operating cost in our business.

- Inherent credit and default risk in our business, particularly trends with sub-groups/ customer segments of the loan portfolio.

- Subventions and subsidies available, if any.

- Risk profile of customer – professional qualification, stability in earnings and employment, past repayment track record with us or other lenders, external ratings of customers, credit reports, customer relationship, future business opportunities etc.

- Nature and value of collateral securities.

- Industry trends – offerings by competition.

Interest Rate Policy for lending business

- The company shall adopt a discrete interest rate policy which means that the rate of interest for same product and tenure availed during the same period by separate customers would not be standardized but could vary within a range, depending, amongst other things, the factors mentioned above.

- The interest rates offered could be on fixed basis or floating / variable basis. Changes in interest rates would be decided at any periodicity, depending upon market volatility and competitor review.

- The interest re-set period for floating /variable rate lending would be decided by the company from time to time, applying the same decision criteria as considered for fixing of interest rates.

- Interest would be charged and recovered on a monthly or quarterly basis. Specific terms in this regard would be addressed through the relevant product policy.

- Interest rates would be intimated to the customers at the time of sanction/availing of the loan and the EMI apportionment towards interest and principal dues would be made available to the customer.

- Interest shall be deemed payable immediately on due date as communicated and no grace period for payment of interest is allowed.

- Besides normal interest, the company may levy additional interest for adhoc facilities, penal interest for any delay or default in making payments of any dues. The levy or waiver of these additional or penal interests for different products or facilities would be described in the sanction letter.

Interest changes would be prospective in effect and intimation of change of interest or other charges would be communicated to customers in a manner deemed fit, as per terms of the loan documents.

- Besides interest, other financial charges like processing fees, cheque bouncing charges, prepayment/ foreclosure charges, part disbursement charges, cheque swaps, cash handling charges, RTGS/ other remittance charges, commitment fees, charges on various other services like issuing NO DUE certificates, NOC, letters ceding charge on assets/ security, security swap & exchange charges etc. would be levied by the company wherever considered necessary. Besides the base charges, the GST and other cess would be collected at applicable rates from time to time. Any revision in these charges would be with prospective effect. These charges would be decided upon collectively by the management of the Company.

- The practices followed by competitors would also be taken into consideration while deciding on interest rates/charges.

- Interest rate models, reference lending rate and other charges and their periodic revisions will be made available for the general public as required.

- In case of staggered disbursements, the rates of interest would be subjected to review and the same may vary according to the prevailing rate at the time of successive disbursements or as may be decided by the company.

- Claims for refund or waiver of such charges/penal interest/additional interest would normally not be entertained by the company and it is the sole and absolute discretion of the company to deal with such requests.

PENAL/ OVERDUE CHARGES:

- The Company may collect a penalty for non-compliance of material terms and conditions of loan contract by the borrower only by way of penal charges and the same shall not be collected as penal interest that is added to the rate of interest charged on the loan amount. Further, late payment fees may be levied on a borrower who fails to make 3 loan due payment by the due date or there is a bounce instance received from the registered bank account for auto debits.

- The penal charges shall not be capitalized by the Company i.e., no further interest computed on such charges. However, this will not affect the normal procedures for compounding of interest in the loan account.

- The Company shall also not introduce any additional component to the rate of interest charged to the borrower and shall ensure compliance with the above.

- The quantum of penal charges shall be reasonable and commensurate with the non-compliance of material terms and conditions of loan contract without being discriminatory within a particular loan/product category.

- The Company shall not, under any circumstances, levy higher penal charges to individual borrowers, who have availed the loan for purposes other than business, than non-individual borrowers for similar non-compliance of material terms and conditions.

- Disclosure requirements: The quantum and reason for penal charges shall be clearly disclosed by the Company to the customers in the loan agreement and most important terms & conditions/Key Fact Statement (KFS) provided to them (pursuant to RBI Guidelines on Digital Lending dated September 02, 2022 and RBI Circular dated April 15, 2024 on Key Fact Statements for Loans and Advances) and the loan agreement. The same shall be displayed on websites of NBFCs under Interest rates and Service Charges.

- Further, whenever reminders for non-compliance of material terms and conditions of loan are sent to borrowers, the Company will communicate the penal charges associated with the same to the Borrower. Any instance of levy of penal charges by the Company shall be communicated to the borrower along with the reason thereof.

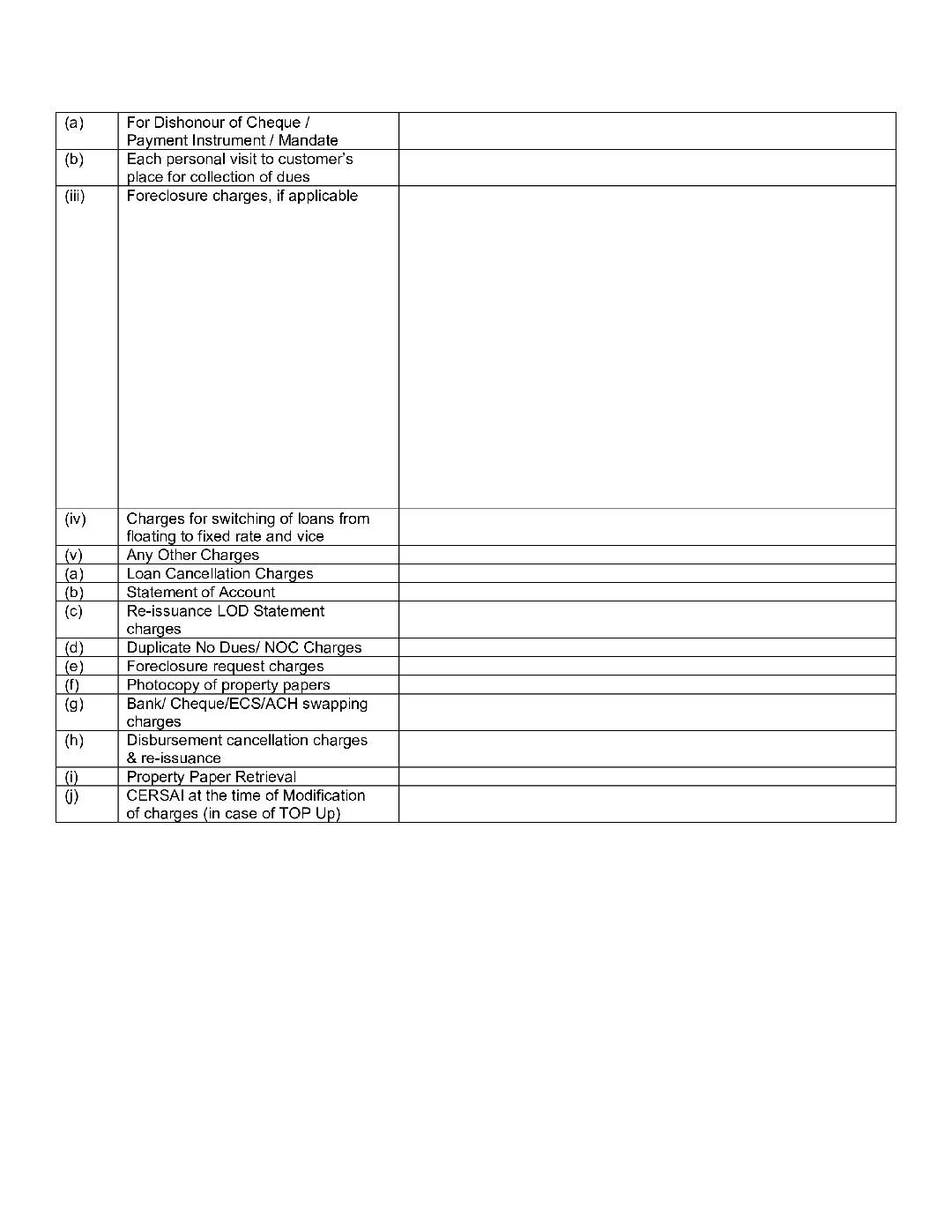

FORECLOSURE / PREPAYMENT CHARGES

In accordance with the applicable guidelines issued by the Reserve Bank of India (RBI), the Company shall levy foreclosure / prepayment charges as under:

-

Floating Rate Term Loans to Individual Borrowers

No foreclosure charges / prepayment penalties shall be levied on floating rate term loans sanctioned to individual borrowers, with or without co-obligants, irrespective of the source of funds used for prepayment.

-

Other Loans (Fixed Rate / Non-Individual Borrowers)

In case of fixed rate loans or loans sanctioned to non-individual borrowers (including entities), the Company may levy foreclosure / prepayment charges as per the terms and conditions stipulated in the respective loan agreement, subject to applicable regulatory guidelines.

-

Disclosure

The applicable foreclosure / prepayment charges shall be clearly disclosed in the sanction letter, loan agreement, and Key Fact Statement (KFS), wherever applicable.

-

Regulatory Compliance

Any changes in regulatory instructions issued by the Reserve Bank of India from time to time shall be automatically applicable and the Company’s policy shall stand modified accordingly.

PROCESSING / DOCUMENTATION AND OTHER CHARGES

The Company generally charges a fee on the loan amount depending on the category of loan and risk associated in the form of processing fees / non-refundable upfront fee. These charges would be decided or revised by the competent product approval committee by way of amendment to existing product approval document.

Other costs and charges such as stamp duty, service tax and other cess would be collected at applicable rates.

All such charges will be disclosed clearly in the loan documentation with the borrower, including in the key facts statement and shall not be charged unless disclosed in the Key Facts Statement (provided pursuant to RBI Guidelines on Digital Lending dated September 02, 2022 and RBI Circular dated April 15, 2024 on Key Fact Statements for Loans and Advances).